Rebooting Investment Management

Oriskany is a creator of quantitative investment strategies, using non-linear datasets and financial engineering to deliver robust, liquid, bespoke investments

Specifications:

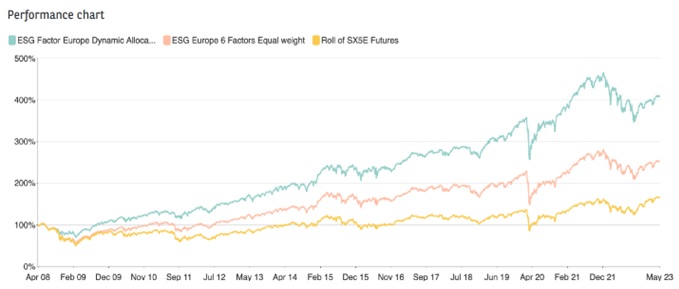

Performance

Source BNP Paribas CIB

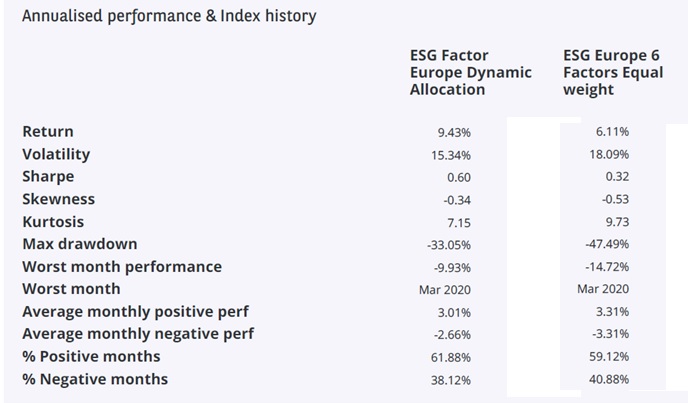

The value creation is spread throughout the life of the strategy and not clustered around a few good “bets”. Overall, with 90% average exposure, the strategy is able to capture most of the upside of a bull market.

Resilience – Controlled Drawdown

[Bouton Vers PDF?]

Source BNP Paribas CIB

Our risk filters are able to capture the increased probability of significant market pull-backs which leads to resilience and the ability to endure downturns. The drawdown is significantly reduced.

Resilience – Fast Recovery

Source BNP Paribas CIB

Because the strategy has controlled drawdowns, it displays on top of its ability to endure, the capacity to recover quickly.

Resilience – Statistically Predictable

Source BNP Paribas CIB

The performance of the strategy is more linearly distributed and the negative tails are reduced when compared to the market, making the strategy easier to predict.

Myth 1: Financial markets are unpredictable, but over time things average out so it is best to diversify and then buy-and-hold.

The unpredictability of financial markets is summarized by the classic “random walk model”, which is based on 3 claims:

The first claim can be accepted, but data and common sense overwhelmingly contradicts the second and third.

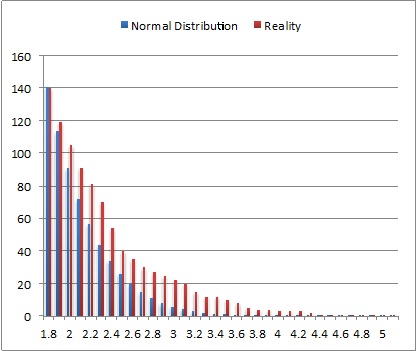

For instance, a histogram of the daily returns of EUR-USD over 6 continuous years shows quite clearly that the bell curve does not hold: the actual number of daily moves of a given magnitude, expressed in numbers of standard deviations (red bars) is far greater than the number predicted by the Normal Distribution (blue bars). In practical terms, this means that extreme outcomes will occur far more frequently than the classical tools (such as VaR) expect. The consequences can obviously be dire…

The assumption of independence of returns from one period to the next is just as problematic. Intuition commands that today’s return on an equity index should have an influence on what happens tomorrow: if the index moved 10% today (up or down), tomorrow is likely to be a volatile day too because the market is nervous. Standard theory refutes this real-life common sense and thus hits a paradox: there might not be a correlation in the direction of the index movements (up doesn’t always follow up), but there is certainly dependence in the magnitude of those moves. Large moves tend to be followed by large moves, it is what B. Mandelbrot calls the “memory” of markets and it helps explain why volatility clusters.

The decision process of financial actors also contradicts the assumption of independence. Because the actions of investors have an impact on the information set they used to decide on these very same actions, a circular reference is created, which will mechanically introduce dependence in the succession of returns. This is what George Soros calls reflexivity.

In a nutshell, price changes do not follow a Random Walk, so it is best not to rely blindly on models that have this assumption at their core (Portfolio Theory, CAPM, Black-Scholes, GARCH models, etc…).

Myth 2: Expected returns and volatility are a good measure of the profile of a portfolio

Standard theory believes that Volatility effectively assesses risk (mean-variance framework of Markowitz). However, intuition and behavioural finance easily contradict this postulate. Indeed, the average stock-market return, around which volatility distributes the outcomes, is of little interest to the real investor, for whom the extremes of profits and especially losses matter much more. Additionally, behavioural finance studies have proven that for a given absolute variation, losses matter far more than profits.

More generally, standard theory has relied extensively on estimates of expected returns, volatilities and correlations to predict the risk of a portfolio. Consequently, this has given rise to the practice of “optimization”, which is a way of choosing the best possible allocations based on those estimates.

This is evidence of over-confidence, a well-known behavioural bias. The world is much more unpredictable than models expect, hence future estimates of volatilities and correlations are bound to be wrong (especially as the time horizon of the prediction lengthens). The optimal solutions are therefore optimal for only one state of the world, and will generally not be robust. Robustness, or the ability of being strong enough to withstand challenges, is much more important: it will determine that a portfolio can perform adequately whatever the environment. In other words, in the rough world of financial markets, it is a waste of resources to fine-tune a Formula 1, better build a robust four-wheel drive instead…

Myth 3: Markets are continuous

Standard theory postulates that quotes and rates do not jump but that they move smoothly from one value to the next. Continuity of this sort characterizes all (physical) systems subject to inertia; it is for instance how temperature moves throughout the day. Newton, Leibnitz, and later the economist Alfred Marshall all believed that “Nature does not make leaps” (Natura non facit saltum), and indeed the human mind is configured to assume continuity, which is a central assumption of MFT. The maths behind the works of Markowitz, Sharpe, Black-Scholes all assume continuity, and without it, the formulae simply do not work.

However, discontinuity and sudden change are everywhere on Financial Markets, from the movements of prices to the expectations of investors. That is where the difference between economics and classical physics is greatest: the supply and demand that determine a price are both functions of objective factors and anticipations. Even if we accept a continuous approximation for the former, the latter can change completely based on a signal that will take very little time and energy. Consequently, we should expect destabilizing jumps and phase transitions as a result.

Rather than applying buy-and-hold strategies that are incorrectly justified by normal distributions and continuous changes, investors are better off using Discontinuity to their advantage by investing in the market much more selectively.

Financial markets have an endogenous life, meaning that, in all places and ages, they work alike. Even if we could isolate the market from its environment completely, there would still be an inherent activity that comes from the way people come together, organize themselves and exchange assets. For instance, in a modeled world where only 2 categories of investors exist (fundamentalists and chartists) and no new information arrives, interactions and variations start to appear spontaneously and bubbles and crashes occur. This instability is intrinsic, and should not be viewed as a simple “deviation from the equilibrium”.